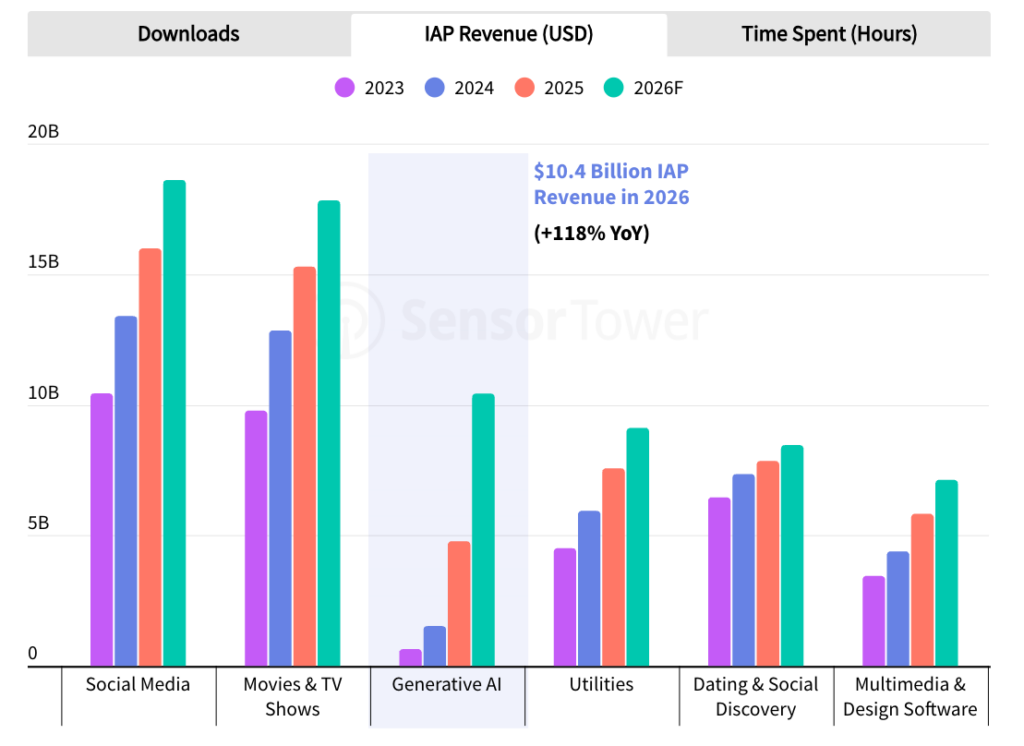

Generative AI was not just the most discussed digital topic of 2025; it became one of the fastest-scaling usage layers ever observed across mobile ecosystems. With applications such as ChatGPT and Google Gemini approaching a combined 4 billion downloads, $4.8 billion in in-app purchase revenue, and 43 billion hours of usage, Generative AI has crossed a decisive threshold: it is now a mass-market behavior, not a niche innovation.

Looking ahead to 2026, the trajectory points to an even more structural shift. In-app revenues and time spent are expected to more than double year-over-year, pushing the category beyond $10 billion and firmly into the top five mobile genres across downloads, monetization, and engagement. This rise is not incremental; it is reshaping the hierarchy of mobile usage itself. ChatGPT alone had already become the #2 app globally by IAP revenue by Q3 2025, trailing only TikTok, raising a credible question: could a generative AI application overtake video as the most valuable consumer app category?

For telecom operators, this is not merely a content trend. Generative AI is a traffic-intensive, latency-sensitive, always-on workload that redefines network value. Time spent in AI applications is expected to surpass entire sectors such as travel, shopping, and financial services, driving sustained demand for connectivity, cloud-edge distribution, and energy-efficient networks.

The strategic question for telcos is therefore clear: will they remain neutral connectivity providers, or will they actively position themselves within the Generative AI value chain, through optimized data plans, AI-aware network slicing, edge inference, device partnerships, or revenue-sharing models with application platforms?

By 2026, Generative AI will not just sit on telecom networks. It will stress, shape, and economically redefine them.

Figures and projections are based on data and estimates from Sensor Tower, including downloads, in-app purchase revenue, and time spent across iOS and Google Play.